Updated on: May 5, 2024

Today I wanted to take a look at two practical examples of how to complete a dividend tax calculation for income based on the 2022-23 tax year. The reason I wanted to do this is because we do have our dividend and salary tax calculator on our website, and you will see various other dividend calculators online that you can use to estimate your tax liability from your dividend income.

However, the shortcomings of these calculators are to do with how dividends are taxed which depends on your other forms of income. It used to be that your dividend income always sat on top of all of your other forms of income when going through the various income tax bands. This meant that your dividend income was always taxed at the highest possible rate. There has been a slight change to this, where you can optimize the amount of personal allowance that gets used in your dividend tax calculation to help reduce your overall tax bill.

Our article Paying Tax of Dividends in 2023/24 talks about how the taxation of dividends works, but a worked example often helps to bed the concepts in.

In the dividend tax calculation examples below, I will cover off two scenarios. The first scenario is for a typical limited company contractor client who received a salary through the limited company of £9,096 per year and received dividend income of £45,000. The second scenario looks at a full-time employee who earns £48,000 per year through their company payroll and also receives £6,000 in dividends. Particularly in the second example, you’ll see how the personal allowance interaction works.

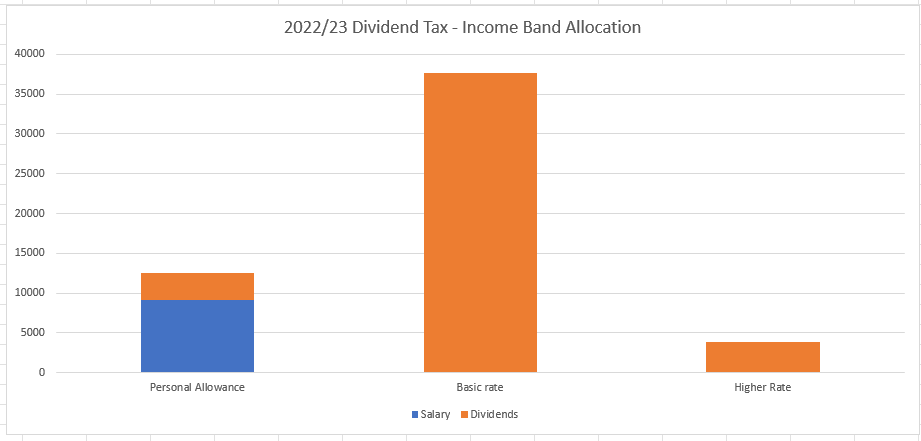

Scenario 1 – £9,096 salary, £45,000 dividends

Here we have a limited company contractor who earns a salary of £9,096 and who also paid themselves £45,000 in dividends for the 2022-23 tax year. As I mentioned in the introduction, the arrangement of a low salary and high dividends is common for limited company contractors. The reason for this is that the salary is a tax-deductible business expense, so it is effectively paid to you tax-free. The remaining amount of dividends gets taxed at various dividend tax rates as we work through the income tax bands.

There is of course the remainder of the personal allowance available after deducting the salary, plus there is the dividend allowance before we start calculating the dividend tax that is due.

So, let’s run through a real-life dividend tax calculation example now using 2022/23 HMRC tax rates and bands.

The personal allowance is £12,570 so the salary of £9,096 comes off this first. This leaves £3,474 of personal allowance that we can use for the dividend income.

So, in the end our taxable dividends are 45,000 – 3,474 = £41,526.

Now we simply run this dividend income through the tax bands. Once the personal allowance has been used up the basic rate tax band handles income of £37,700. Because we have taxable dividends of £39,526, this tax band gets fully used up with dividend income. However, the first £2,000 of this (the divided allowance) is tax free. The remainder of the dividend income (41,526 – 37,700 – 2000) = £3,826 gets taxed within the next tax band which is called the higher rate income band.

So, in this case the summary of our dividend income tax calculation is;

Personal allowance 3,474 (untaxed)

Basic rate dividend income, 2000 @ 0% = 0 (this is the dividend allowance)

Basic rate remaining dividend income, 35,700 @ 8.75% = 3,124

Higher rate dividend income 3,826 @ 33.75% = 1,291

Total dividend tax liability for 2022/23 = £4,415.

Below you can see how the income is spread across the first three income tax bands.

This is a very simple example that shows you how a dividend tax calculation works in its most basic form. If our contractor were to have another form of income such as property rental income then the overall the dividends would be taxed at a higher rate because the rental income would be using up some of the basic rate tax band, which would in turn push some of that dividend income into the higher rate tax band.

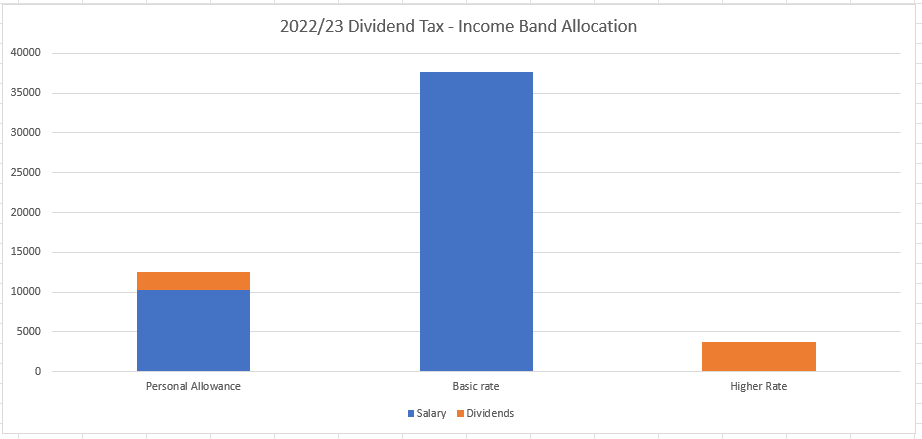

Scenario 2 – £48,000 salary, £6,000 dividends

In our second dividend tax calculation scenario, let’s take a look at a full-time employee who earns £48,000 per year. The income is paid to this employee every month and is taxed through the usual payroll system by their employer. Normally, this employee would not need to file a UK personal tax return because all of their income so far is taxed already.

However, let’s introduce £6,000 of dividends to this scenario. The dividend income might come from investments, or it might come from a private limited company they have shares in. For the purposes of the dividend tax calculation, it makes no difference where the dividend income comes from. Now, because our employee now has a form of untaxed income which exceeds the dividend allowance of £2,000, they are now required to file a personal tax return.

Normally in this situation you would expect the salary to use up all of the personal allowance and all of the basic rate income band, and that the taxation of dividends sits on top of this salary income. However, you are allowed to adjust the make-up of how your personal allowance is used, and HMRC approved personal tax return software will automatically do this for you.

In this particular case it is optimal to have all of the salary income taxed at the basic rate limit because this pushes all of the dividend income into the higher rate tax band, of which the first £2,000 (dividend allowance) is tax free.

In this case we use £10,300 of the personal allowance for salary, along with the full basic rate tax band of £37,700 and combined, this accounts for the full salary of £48,000.

This means for our dividend income we have a personal allowance of £2,270 that we can use (12,570 less 10,300), we have no basic rate tax band available to us, and all other dividend income is taxed at the higher rate band.

So, in this case the summary of our dividend tax calculation is;

Personal allowance 2,270 (untaxed)

Basic rate dividend income, 0 (all used up with salary)

Higher rate dividend income, 2,000 @ 0% = 0 (this is the dividend allowance)

Higher rate remaining dividend income, 1,730 @ 33.75% = 584

Total dividend tax liability for 2022/23 = £584.

Below you can see how the income is spread across the first three income tax bands.

You will be right in thinking that a dividend tax liability of £584 it’s quite small for dividend income of £6,000.

The interesting thing about this scenario is with a £48,000 salary, and assuming this employee was on the usual 1257L tax code, their employer would have deducted £7,084 in tax from their salary. This would have been based on the assumption that the employee had the full £12,570 personal allowance available to be used for the salary income. However now that dividends have been introduced into the scenario, and using the optimised dividend tax calculation above, that same salary now must be taxed at £7,540.

Overall, what this means is the personal tax bill for this employee will now be a combination of both the dividend tax and the extra salary tax which in this case equals £1,040.

This now makes a bit more sense with the overall tax liability faced by the employee as a result of receiving £6,000 in dividends now being £1,040.

Summary

You can see from these two scenarios that the taxation of dividends isn’t as straight forward as plugging a number into an online dividend tax calculator. There are numerous factors to be considered and as you’ve seen in scenario two, you are allowed to optimise the use of your personal allowance for the best possible dividend tax calculation result.