Updated on: Mar 26, 2024

In this guide we take a look at the HMRC P11D form. It’s not highly used by our clients (and we will explain why below) however as accountants we need to have an awareness of the P11D and the circumstances that it must be used. It is one of those forms that can easily fall off the radar, as its submissions and payment deadline is completely separate to any other HMRC reporting requirements. Here we will take a look at what the P11D is, when it is due, and how to fill it out correctly, and how to file it online with the HMRC.

At No Worries we take care of all P11D and P11D(b) reporting requirements for our clients where this is necessary.

What is the P11D Form?

The P11D Form is a form used by employers in the UK to report certain fringe benefits, such as expenses and benefits-in-kind, which are provided to their employees. These are items that are paid in additional to normal salary such as private healthcare, interest-free beneficial loans, employer provided living accommodation, and company cars.

It’s important to note here that it’s typically the expenses and benefits paid by the employer where;

(a) the employer has the liability to pay, and

(b) pays directly from the business bank account to the supplying firm, that are reported on the P11D.

If an employee has their own medical insurance that was set up by themselves, and the employer reimburses them for this cost, this is not a P11D reportable expense. Instead, the employer must ensure that this reimbursement is processed through payroll with the appropriate deductions for PAYE and National Insurance.

The P11D is used to ensure that non-cash benefits or perks provided to employees do not escape tax. The tax bill liability of the P11D is paid by the employer based on the taxable benefits enjoyed by the employee. Plus, the value of the tax benefit is reported (and taxed) on the employees personal tax return. Not all benefits provided to employees are taxable, with relevant life cover being an example.

The overall intention is to pay tax on non-cash benefits at a similar rate to wages and salary. For the vast majority of our limited company contractor clients, their tax position needs to incorporate an overview of both company and personal taxes. For this reason, the P11D (which introduces a new form of tax for your business, in addition to corporation tax) means there is little to no benefit in paying expenses and benefits enjoyed by the Director from the company bank account.

For the vast majority of our limited company contractor clients, there is very little tax benefit in making these benefits-in-kind payments throughout the tax year, so the P11D form does not need to be completed. However, we do have a small number of clients who file a P11D each year and its mainly because they have

(a) a company vehicle, or

(b) medical insurance, that is paid for by their limited company.

The P11D is a two-page document that must be completed in full and submitted on time. Failure to submit the form, or to submit it accurately, can result in fines, and penalties. It is important to understand the contents of the form, so you can be sure that you are filing it correctly.

What is included in the P11D Form?

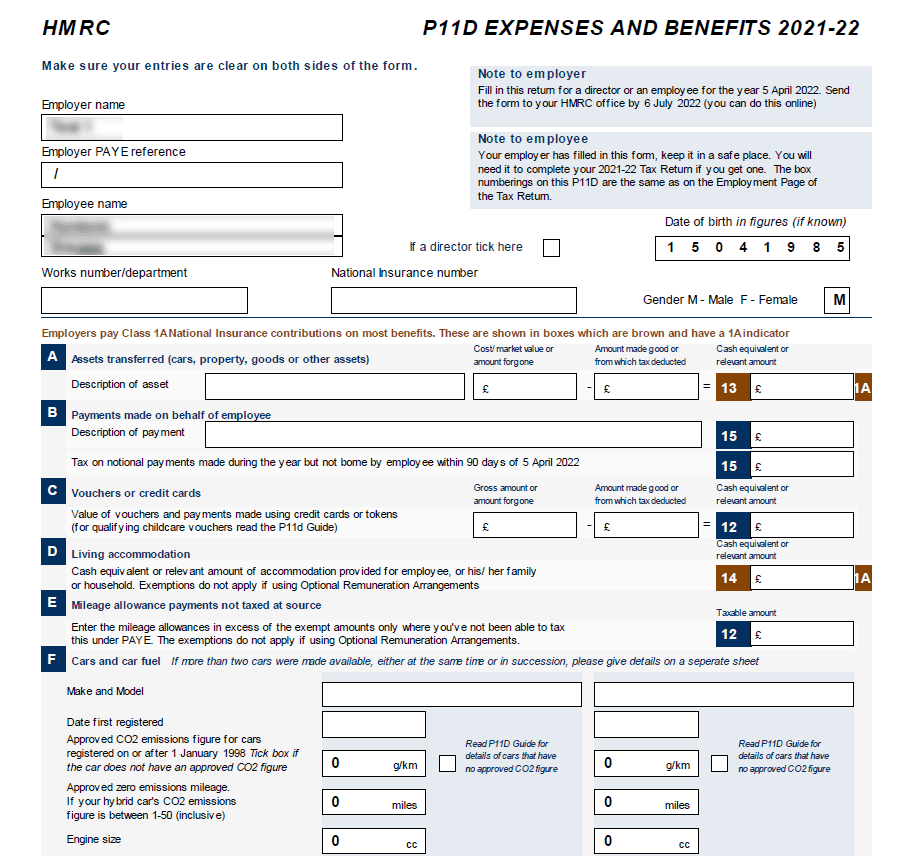

The P11D Form is divided into 14 sections, each of which includes specific information about the employee’s benefits and expenses. The top of the form requires the usual employer and employee information such as the employers name and PAYE reference number, and the employees name, date of birth, and NI number.

The form then contains 14 sections as listed below. Having a read through these sections you will see the typical items that need to be reported on the P11D. An excellent resource to help you with this is the HMRC Expenses and benefits: A to Z guide, which identifies a large number of typical expenses along with the conditions required take makes them taxable benefits that must be reported in the P11D.

a. Assets transferred (cars, property, goods or other assets)

b. Payment made on behalf of employee

c. Vouchers and credit cards

d. Living accommodation

e. Mileage allowance payments not taxed at source

f. Cars and car fuel

g. Vans and van fuel

h. Interest free and low interest loans

i. Private medical treatment or insurance

j. Qualifying relocation expenses payments and benefits

k. Services supplied

l. Assets placed at the employees disposal

m. Other items (including subscriptions and professional fees)

n. Expenses payments made on behalf of the employee. This includes travelling and subsistence payments, entertainment, payments for use of home phone, non-qualifying relocation expenses, other expenses.

What is the Difference Between the P11D and P11D(b) Forms?

The P11D is used to report the benefits and expenses provided to employees. The P11D(b) form is used to report the employer’s Class 1A National Insurance Contributions due on these benefits and expenses. Think of the P11D(b) as a tax summary of all the P11D’s that were created by the employer.

While each employee requires their own P11D, the P11D(b) form is for the employer and is simply a summary of the Class 1A national insurance tax liability that is due based on the information that is contained within the P11D’s for each employee.

All tax software products we have used for preparing P11D’s also integrate the P11D(b) reporting, which makes the preparation of the forms and filing simple.

The HMRC’s Online End of Year Expenses and Benefits service is provided for free, and can also file the company P11D(b) form online.

When is the P11D Due?

The P11D is due to be submitted to the HMRC by the 6th of July following the tax year in which the benefits were provided. For example, if the benefits were provided in the 2022/23 tax year, then the P11D must be submitted by the 6th of July 2023.

It is important to note that the P11D must be submitted in full, with all the relevant information included, by the due date. Failure to submit the form on time can result in fines and penalties. Remember that the P11D(b) form must also be filed at this time, which reports the Class 1A NIC that is due to be paid by the company.

The deadline for payment of Class 1A NICs is 19 July, or 22 July, if paid electronically.

How to Fill Out the P11D Form

Filling out the P11D can be a large task for employers, however if your accounting and payroll records are up to date, all the information you require will be close at hand. If your information filing and storage system is a little more haphazard, pour yourself a nice coffee and then prepare to spend several hours digging out all the information you need.

The first step is to ensure that you have all the necessary information about the employee’s benefits and expenses. The basic information will be easy to collect such as their name, address, and national insurance number. The details of any benefits-in-kind or expenses paid for by the employer maybe be harder to collect. Some software products allow you to tag company expenses as P11D-able, so you may be able to get a report of this information quite quickly.

Also remember to look at previous years P11Ds to ensure you are capturing any relevant historical benefits that still need to be reported (such as the provision of a motor vehicle).

Once all the relevant information has been gathered, it is time to fill out the form. The form is divided into sections, each of which requires specific information. It is important to ensure that all the information is provided accurately, and that you have a record of information and calculations that back up your reported data.

How to Submit the P11D Form

Once the P11D has been completed, it must be submitted to the HMRC. There are two ways to do this: by post or online.

The easiest and most efficient way to submit the P11D is online. To do this, use your payroll software (note, not all payroll software has a feature to file P11D’s) or else use the HMRC End of Year Expenses and Benefits service which is provided for free. The online service the HMRC run for filing payroll (and P11D’s) is open all year round.

Alternatively, you can submit the form by post. To do this, you will need to print out a copy of all the P11D’s that need to be filed, along with the P11D(b), fill then in, and post it to the HMRC. This would have to be a worst-case scenario though, and in 2023 I cannot envisage a scenario where you need to post in your returns.

What to Do If You Make a Mistake on the P11D Form

Making a mistake on the P11D can happen. Once the mistake is picked up you can file amended returns to correct the error. But note that you may have to pay a penalty if you carelessly or deliberately give inaccurate information.

The issue here is, once the mistake is picked up, the amended returns cannot be filed via HMRC’s PAYE online service and can ONLY be resolved by filing paper P11D forms with the HMRC, (ie posted). In most cases your payroll software will allow you to print off your P11D for P11D(b) forms which makes things easier, however we suggest you also add a covering letter to explain the mistakes that were picked up. Note that the re-submitted forms must be a complete re-filing all ALL P11D expenses and benefits (not just the amendments).